Welcome to San Diego Blog | October 31, 2019

Housing Bubble?

Nope – No Bubble

Many buyers are sitting on the sidelines in anticipation of a major housing downturn even though the facts illustrate it simply is not going to happen.

No Bubble: Housing data illustrates that there is not a housing bubble on the horizon.

It has happened to just about everybody. Driving down the road, unaware of your current speed, a look in the rearview mirror reveals there’s a police car with sirens blazing pulling you over. After receiving the ticket and driving away, for quite some time your driving habits change. You are more cautious, more aware of your surroundings, anticipating at any moment that, inevitably, you will be pulled over again.

Similarly, so many buyers and homeowners are mentally preparing for the next housing bubble to pop. Everybody knows somebody that was affected by the Great Recession when values dropped substantially and countless homeowners lost their homes to foreclosures or short sales. With values surpassing record levels, isn’t housing in a bubble again? Even though so many are anticipating another bubble, the answer is simple: NOPE.

The Great Recession was prompted by the housing market where anyone could purchase a home regardless of their true qualifications. Zero down payment loans, fudged loan documents, negative ARMs, cash-out financing, and subprime lending contributed to the run-up in values that filled the housing bubble that ultimately burst in 2007. As a result, the housing market collapsed, and home values plummeted.

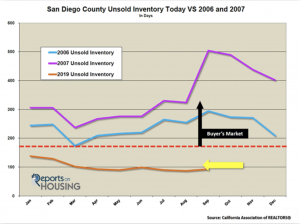

The writing was on the wall prior to the collapse. Housing data illustrated market conditions that were lining up in favor of buyers. The inventory ballooned while demand crumbled. As a result, the unsold inventory rose to ridiculous heights. The numbers were off a year prior to the subprime meltdown, which occurred in March 2007. In 2006, the unsold inventory surpassed 180 days (a Buyer’s Market) in April. In 2007 it remained above 180 days all year and surpassed the 300 day level in June. In September, it even eclipsed 500 days.

Flash forward to 2019, and the unsold inventory has remained between 80 and 140 days, a slight Seller’s Market, one where there is not much appreciation and sellers get to call more of the shots during negotiations. Today, smack dab in the middle of the Autumn Market, it is at 93 days. And for the rest of the year do not expect it to change much.

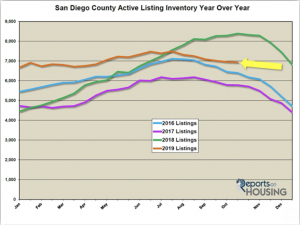

The big difference is supply and demand. Currently, the active listing inventory is at 6,932 homes. Back in 2006 there were over 15,000 homes and in 2007 there were over 18,000 homes on the market, nearly three times today’s supply. Current demand (the last 30 days of pending sales) is at 2,850. In 2006 and 2007 demand was less than 2,000. With a supply of homes through the roof and weaker demand, unsold inventory reached very high levels prior to the Great Recession and strongly indicated that housing values would slide massively.

It is also important to note that it is much more difficult to obtain financing today. Buyers must qualify for a loan and furnish paperwork that establishes their ability to make their monthly payments. There is no more “easy money.”

The housing market is not as hot today as it was from 2012 through 2017, but that does not mean that the housing market is in a bubble. Demand is only slightly sluggish today and the active listing inventory is dropping fast. The storyline since 2012 is that there has been a supply problem, not enough homes on the market. The story is true today and will continue in 2020. And, the low interest rate environment with mortgage rates below 4% has substantially helped home affordability and will fuel the housing market for quite some time.

The housing market is not as hot today as it was from 2012 through 2017, but that does not mean that the housing market is in a bubble. Demand is only slightly sluggish today and the active listing inventory is dropping fast. The storyline since 2012 is that there has been a supply problem, not enough homes on the market. The story is true today and will continue in 2020. And, the low interest rate environment with mortgage rates below 4% has substantially helped home affordability and will fuel the housing market for quite some time.

The bottom line: today’s housing data illustrates a housing market that is on very strong footing. There is no bubble. The inventory is low, buyer deman is not weak, the Expected Market Time is low, and mortgage rates are at historically low levels.

Re-printed with permission from Steven Thomas, Quantitative Economics and Decision Sciences, B.A.

Contact me for more information and accompanying data!

Written by: Arlis W. Travis

Categories: Absorption Rates, Market Conditions, Market Trends, Real Estate Tips for Buyers