Welcome to San Diego Blog | April 9, 2021

San Diego County Housing Report: Waiting Will Be Costly

Even though buyers are exceedingly frustrated with the housing market after writing too many offers to no avail, waiting until the market gets easier is not the answer.

Cost of Waiting

Housing will become more unaffordable as homes continue to rapidly appreciate and mortgage rates rise.

Ask any buyer what it is like attempting to purchase a home in today’s housing market and the responses will be the same. It is frustrating, overwhelming, exhausting, and disheartening. Buyers consistently get their hopes up and run around each weekend to see the few new houses that are now available. They ultimately write another offer. A few days later they write a counteroffer, often for way more than the asking price. They agonizingly wait another day or two only to find out that they are not the winning bidder. It is back to the drawing board, again.

It feels like a dog chasing its own tail, a pointless exercise that ends in exhaustion. After writing offer after offer with no success, many buyers become discouraged and question whether they should continue to pursue their dream of purchasing a home. Maybe they should wait until the market is not so blistering hot, or until they have a larger down payment, or when there are more homes available. The facts and data illustrate why waiting is not a great strategy at all.

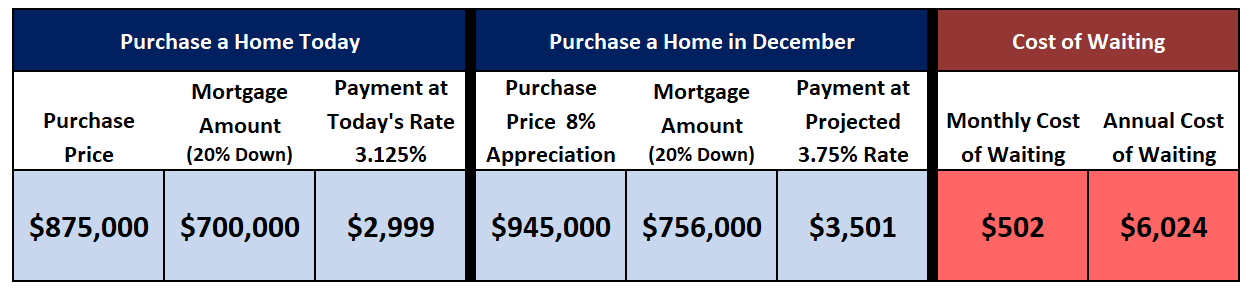

While it may be discouraging for buyers to continue the pursuit of purchasing a home, diving into the consequences of waiting will keep them motivated. It is important to focus on the monthly payment in purchasing a home today and compare it to delaying until the end of the year. An $875,000 home purchased today with a 20% down payment yields a monthly payment of $2,999 at the current interest rate of 3.125%.

With a record-low supply of available homes to purchase paired with unstoppable demand powered by historically low mortgage rates, home values are anticipated to continue to increase at a pace of about 1% per month through the end of the year. That equates to a home appreciation of 8% from now through December. At the same time, the United States economy is revving its massive engine now that it is emerging from the depths of the pandemic. Excellent job reports, increased travel, a massive personal savings surplus, and a return to some semblance of normal life again will ignite the economy and translate to a rise in mortgage interest rates. It is already occurring. According to Freddie Mac’s Primary Mortgage Market Survey®, rates started the year at 2.65%, an all-time record low, and have since risen to 3.125%. That is nearly half a point higher in just a few months. By year’s end, rates are forecasted to hit 3.75% or higher.

That means that the $875,000 home example above will appreciate $945,000 in December. Match that up with the expected 3.75% mortgage rate, and the monthly payment blossoms from $2,999 to $3,501 per month, an increase of $502 every single month for the life of the loan. That is $6,024 per year or $30,120 in five years. This example only factors in the increase in the principal and interest payment. The 20% down payment for $945,000 is an extra $14,000 down. Property taxes go up too. With the average tax rate of 1.1%, that amounts to an additional $770 annually.

In the end, it all adds up to a lot more out-of-pocket expense on waiting until the end of the year to pull the trigger on a purchase. There is a definite cost to waiting even though the current market is extremely frustrating from a buyer’s perspective. There is a higher monthly mortgage payment. Down payments are larger. Property taxes are higher.

There are some who believe that when rates rise to 3.75% that the housing market will reverse course and become a buyer’s market. There are plenty of YouTube videos that promote this explaining that a 1% rise in rates translates to a 10% drop in prices. Yet, that did not occur in 2013 when rates rose from 3.34% in January to 4.5% in July. It did not occur in 2018 when rates rose from 3.95% in January to 4.94% in November. Home prices did not fall. These theories are not rooted in fact. Instead, they are click bate for views, after all, that is how YouTubers are paid.

It is better to look at supply and demand. While demand will decrease when rates rise to 3.75% or 4%, it will not shut off demand completely. It will still be a Hot Seller’s Market. It would be like decelerating on the freeway from 140 miles per hour to 80 miles per hour. While it may be slower, it is still speeding. Housing will move from a crazy, nutty market to a more sustainable pace.

The current number of available homes to purchase is at a record low of 2,175. The five-year average (from 2015 to 2019 and intentionally excluding 2020 as the numbers were skewed due to the pandemic) is 5,999, or 176% more. That is an extra 3,824 homes on the market. Current demand (a snapshot of the last 30-days of pending activity) is at 3,352 compared to the five-year average (2015 to 2019) of 3,581, or 6% less. The only reason it is less is that 19% fewer homes came on the market during the first quarter of 2021, which is 2,573 missing FOR-SALE signs. Today’s trend in housing is an ultra-low supply of available homes matched up with fiery, hot, insane demand. With rising rates, the inventory will finally rise from its unparalleled, anemic low level, and demand will decline from its torrid pace. The result will be a market that is much more manageable to navigate, yet still a Hot Seller’s Market. Homes will still appreciate, just not at its current unparalleled pace. There will still be multiple offers, just a few generated on each property compared to the double digits of today.

For buyers, the answer is simple, do not wait to purchase. Waiting will be costly.

Courtesy of Steven Thomas, Reports On Housing.

Written by: Mia

Categories: Market Trends